| |

|

|

|

|

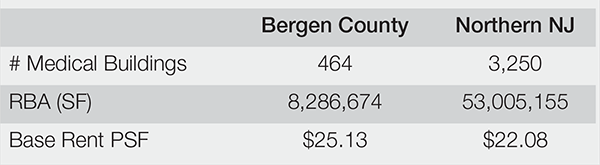

Northern NJ

3,250 Medical Buildings

53,005,155 SF RBA

$22.08 PSF Base Rent |

|

Bergen County

464 Medical Buildings

8,286,674 SF RBA

$25.13 PSF Base Rent |

|

|

|

|

|

|

|

|

|

|

|

SALES

154,089 SF | $62,210,000 95 Madison Avenue, Morristown, NJ Buyer: Atlantic Health Systems Seller: G-A Healthcare REIT III

22,000 SF | $10,500,000 1081 US-22, Bridgewater, NJ Buyer: Kings Row Medical Props LLC Seller: Michael E Pollack |

|

LEASES

12,900 SF 1450 US Highway 22 W Mountainside, NJ

11,667 SF 290 W Mount Pleasant Avenue Livingston, NJ

9,000 SF* 5 Franklin Avenue Belleville, NJ |

|

|

|

*Team Lizzack-Horning Transaction

|

|

|

|

|

|

|

|

|

|

Economic circumstances have little impact on illness, chronic health conditions, injuries or other health concerns. Patients still need treatment even during downturns, so the demand for medical services tends to remain stable. This resilience has allowed the medical office sector to consistently provide high returns with minimal volatility across cycles.

For example, medical office building (MOB) demand remained high throughout the COVID-19 pandemic, with vacancies holding at pre-2020 levels. As a result, medical offices still offer the most favorable long-term, risk-adjusted returns among major property types.

By the Numbers

Healthcare represents over 17% of the U.S. GDP, with outpatient care and medical offices comprising a significant portion. The sector has shifted toward a retail mindset, with systems and providers attracting new patients and expanding into new areas, fueling demand for quality medical space.

Landlords benefit from tenants signing long (15 to 20-year) leases and typically renewing at 80% or higher rates to maintain patient access. Rent growth runs 2-3% annually, enabling stable fundamentals through cycles. Occupancy rates have also risen as absorption outpaced new supply — those rates topped 92% in 2023.

By the end of Q4 2023, these were Bergen County and Northern NJ numbers, with rents dropping a few pennies per square foot. |

|

|

|

According to the 2024 Emerging Trends in Real Estate report from PWC and the Urban Land Institute, investment volumes slowed from a 2022 peak of $30B to $20B in mid-2023. However, transaction activity remained consistent with 2018-2021 levels. Distress is limited, though a pricing disconnect has temporarily reduced deal volume. With over 1.5B SF of inventory, substantial opportunity remains for investors.

Looking Ahead to 2024 Although the office market faces challenges, the MOB component remains solid and resilient. They benefit from a steady base of tenants and patients, long lease terms and limited new supply. Moreover, an aging population, expanded access from healthcare access reforms and medical advances enabling more outpatient procedures support increased demand.

Over half of the medical office space is physician or hospital-owned. Institutional players often partner with specialized operating firms adept at acquiring and managing facilities aligned with health systems. Speculative development is rare and limits growth to 1-2% annually based on tenant needs. The PWC and Urban Land Institute report recommends buying or holding the vector, citing fair pricing, as MOBs have matured into an attractive, stable CRE asset class. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Teterboro, NJ | 201 488 5800 Parsippany, NJ | 973 463 1011 |

|

|

|

|

|

|

|

|

|

|

|

|

.png)