| |

|

|

|

|

Northern NJ

3,220 Medical Buildings

52,293,886 SF RBA

$21.84 PSF Base Rent |

|

Bergen County

458 Medical Buildings

7,896,814 SF RBA

$25.41 PSF Base Rent |

|

|

|

|

|

|

|

|

|

|

|

SALES

154,089 SF | $62,210,000 95 Madison Avenue, Morristown, NJ Buyer: Atlantic Health Systems Seller: G-A Healthcare REIT III

20,554 SF | $4,620,000 10 James Street, Florham Park, NJ Buyer: Desai Holdings; Shreekesh Desai Seller: Silverman Group |

|

LEASES

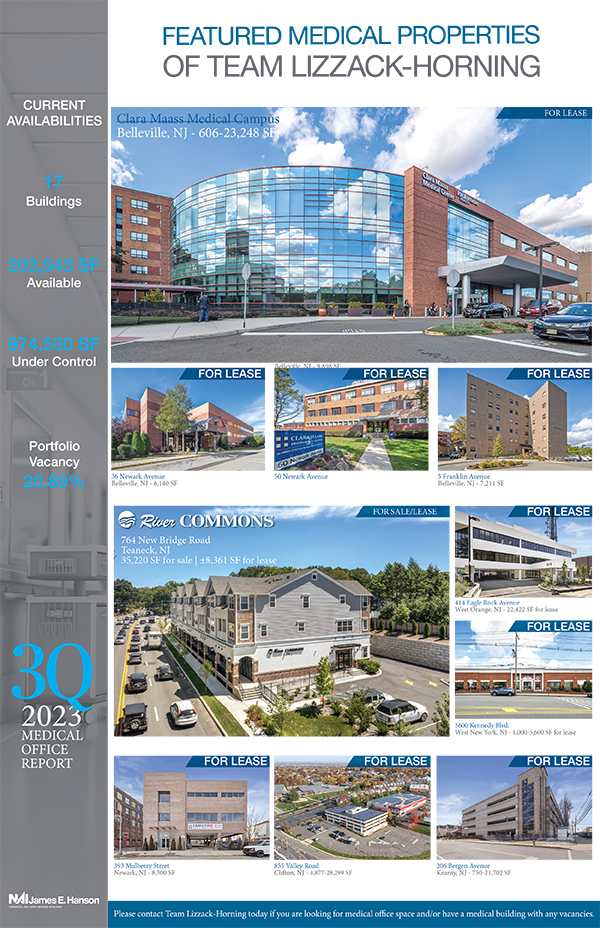

9,000 SF* 5 Franklin Avenue Belleville, NJ

3,884 SF* (Renewal) 36 Newark Avenue Belleville, NJ

2,238 SF 401 Hamburg Turnpike Wayne, NJ |

|

|

|

*Team Lizzack-Horning Transaction

|

|

|

|

|

|

|

|

|

|

The healthcare sector is performing well this year despite some challenges posed by rising interest rates, inflation, and market uncertainty. Medical office buildings (MOBs) remain the most popular type of investment, with occupancy rates and asking rents at record highs. Ambulatory surgery centers (ASCs) are also in high demand as more healthcare providers move surgical procedures to outpatient settings.

Other types of healthcare real estate performing well this year include: - Behavioral health facilities

- Rehabilitation centers

- Senior housing

- Skilled nursing facilities

- Telehealth facilities

Despite some challenges, the long-term outlook for the healthcare CRE market is positive. The sector is traditionally recession-proof, making it an attractive investment for investors seeking stability.

Effects of Capital Markets on Healthcare Construction High interest rates continue to increase costs for borrowing money to pay for construction projects, leading to delays and cancellations as healthcare providers become more cautious with their investments.

Inflation is also driving up labor and materials costs, creating challenges for healthcare providers to budget for — and complete — projects on time and budget. Volatility in the stock and bond markets are additional pain points as investors become more risk-averse, making it difficult for healthcare providers to raise capital for current and future construction projects.

Despite these challenges, many factors support healthcare construction in 2023. - An aging population is driving demand for healthcare services and creating a need for new and expanded facilities.

- The shift to outpatient care — ambulatory surgery centers, medical office buildings, and other facilities — is also creating opportunities.

- The Inflation Reduction Act of 2022 incentivizes healthcare providers to invest in energy-efficient building systems, which can help offset some of construction’s rising costs.

Specific examples of capital markets’ impacts on healthcare construction this year include: - The University of Pennsylvania Health System announced in June that it was delaying a $1.5 billion expansion project due to rising interest rates.

- In August, the California Hospital Association reported that its members were facing an average 20% construction cost increase driven by inflation.

- The healthcare real estate investment trust HCP announced in September that it was reducing its investment guidance for 2023 due to market uncertainty.

|

|

By the numbersOverall, the sector is performing well this year, with demand for healthcare facilities projected to grow in the coming years driven by an aging population, a shift to outpatient care, and an increasing prevalence of chronic diseases.- Medical property sales during the first half of 2023 were $3.1 billion, lower than the same period in 2022’s $9.2 billion but aligned with similar declines in multi-housing and office properties — followed by hotel, industrial, and retail sectors averaging 50% sales volume declines.

- The number of MOB properties exchanged YTD is down 15.6% compared to the first half of 2022.

- MOB portfolios declined from $4.6 billion in the first six months of 2022 to $316 million over the same period in 2023.

- The 2023 average cap rate on MOB transactions has hovered at 6.5% — up 60 basis points since 2022.

- Single asset trades dropped from $4.6 billion in 2022 to $2.8 billion in 2023.

Bergen County and Northern NJ numbers for Q3 2023:

Bergen County - 458 medical buildings

- 7,896,814 SF RBA

- $25.41 PSF base rent

Northern NJ - 3,220 medical buildings

- 52,293,886 SF RBA

- $21.84 PSF base rent

Team Lizzack-Horning’s year-to-date statistics include 16 leases totaling 58,642 SF. The average rents start at $28.41 PSF MG, with average rents during the term at $31.85 PSF MG and an average lease term of 6.8 years.

Looking ahead to Q4 and 2024 Medical properties remain a good investment for investors because they have a durable income profile with long-term leases from strong healthcare tenants, often investment grade rated, with predictable cash flow and rental escalations. Both institutional sources and private capital are attracted to this investment.

Market disruption has slowed deal velocity as participants adjust pricing expectations, which makes sense, given that benchmark interest rates for financing have increased 50 to 100 basis points since January, the forward yield curve indicates a higher-for-longer outlook, and commercial banks — a critical source for financing healthcare properties — may be restricting their lending due in large part to increased regulation. Medical properties remain an attractive option for investors seeing certainty and inflation protection.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Teterboro, NJ | 201 488 5800 Parsippany, NJ | 973 463 1011 |

|

|

|

|

|

|

|

|

|

|

|

|