| | | | | | Northern NJ

3,147 Medical Buildings

50,804,977 SF RBA

$22.10 PSF Base Rent | | Bergen County

442 Medical Buildings

7,174,944 SF RBA

$25.41 PSF Base Rent | | | | | | | | | | | | SALES

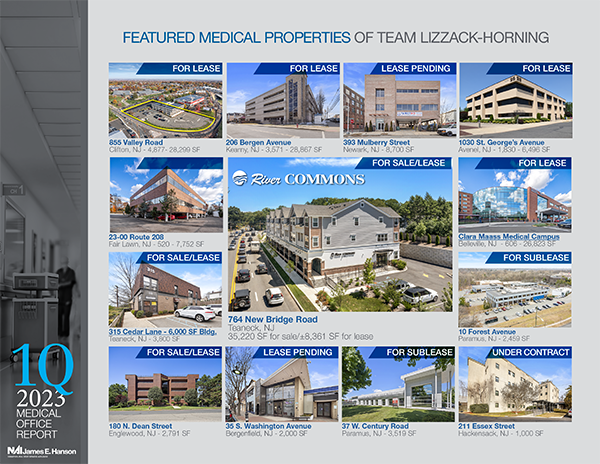

26,150 SF | $4,200,000 330 Changebridge Road, Pine Brook, NJ Buyer: National Retail Properties Seller: South Salem Street Associates

6,270 SF | $1,350,000 37 E. Willow Street, Millburn, NJ Buyer: Somma Associates, LLC Seller: Michael Adler | | LEASES

22,014 SF | 500 N Franklin Turnpike, Ramsey, NJ

16,000 SF | 515 Union Boulevard, Totowa, NJ

12,954 SF | 155 Passaic Avenue, Fairfield, NJ*

*Team Lizzack-Horning Transaction | | | | | | | | | | | |

As 2022 wound down, investors predicted that while economic conditions remained turbulent, the healthcare and life sciences industry would see more dealmaking in 2023. An early 2023 report said 60% of healthcare and life sciences investors intended to engage in M&A activity. Other experts predict the M&A volume will increase throughout 2023, although continued high interest rates and global economic instability are influencing investors to proceed with caution.

- Volume will increase in the second half of 2023. Current high-interest rates and valuation misalignment between buyers and sellers may slow deals in Q1 and Q2. This slower pace will increase interest in more creative financing structures like co-investments, minority recapitalizations, a return to earnouts, and seller financing.

- The specialty outlook is good. Cardiology, GI, oncology, ortho/PT and other specialty physician practices remain popular. One reason? Evolving — and accessible — technology has reduced risk and improved patient outcomes. Technology has enabled physicians to perform 50% of cardiac treatments in outpatient settings, for example.

Specialty practices like these also generate opportunities to aggregate huge volumes of clinical data which biotechnology and pharmaceutical companies are monetizing as they develop new treatments.

| |

Smaller for-profit companies and larger health systems have also asked for full risk. The result? More robust workflows that enable providers to more effectively manage patients, resulting in fewer hospital visits, acute episodes, or readmissions. Another result? This full-risk arrangement reduces the costs shared amongst companies, payors, and practices — and increases patient satisfaction.

Digital health growth has slowed since its initial explosive momentum, accelerated by the pandemic. But rising costs of face-to-face healthcare, ongoing staffing shortages, and the ability of telemedicine to reach people who otherwise have limited access to the care they need has secured analytics, health tech and telehealth companies’ roles as attractive assets this year.

Behavioral health continues to become specialized. With digital health providers expanding their scope of care to include behavioral health, experts predict this currently fragmented market — comprised of informal private practices — is ripe for consolidation. Tele-mental health providers may increasingly focus on acquiring assets in condition-specific behavioral sciences like ADHD, PTSD, and OCD as well as group therapy practices.

Investors have suggested there are several main obstacles to M&As: continued inflation and additional higher interest rates; strong competition for tempting targets; and anticipated impact on the economy.

But a PwC analysis counters, suggesting that increasing transaction volumes and players embracing value-based care — coupled with large levels of corporate cash and private equity dry powder — are leading to continued expansion for deal volumes in 2023. Deal volume will remain robust and resilient despite headwinds.

Many CRE professionals believe the data supports the reputation for resilience that the healthcare and life sciences industry has established. Other reports say competition from generics and biosimilars, a growing gene therapy pipeline, the loss of patient exclusivity, increased patient awareness, expectations and requirements, and breakthroughs in digital technologies will increase M&A activity this year, too.

| | | | | | | | | | | | | | | | | | | | | | Teterboro, NJ | 201 488 5800 Parsippany, NJ | 973 463 1011 | | | | | | | | | | |